When you hear the word “cereal,” there are some obvious connotations that come to mind.

Turn on the Saturday morning cartoons, and pour milk over a bowl of sugar-laden Fruit Loops or Frosted Flakes. Nostalgia in a 12 x 8-inch box.

But cereal has hit headwinds in recent years. Supply chain issues, changing consumer habits, and a pandemic, among other problems, have meant the two or three cereal makers that dominate the market are facing flat sales.

Despite that trend — or more likely because of it — a bundle of upstarts have collectively raised more than $100 million to take on Kellogg’s, General Mills, and Post. To do it, they’re leaning on the DTC approach to quickly gain traction with young consumers. As part of our Mystery Shopper series, we’re taking a close look at three of these: Magic Spoon, Schoolyard Snacks, and OffLimits.

But first, we’re going to take a look at the market they’re trying to disrupt. Grab your spoon and dig in.

The State of Cereal

What you may think of as “cereal” (a wheat or corn-based product dropped into a bowl with milk) is typically referred to as “ready to eat (RTE) cereals.” It’s an important distinction considering the first cereal needed to be soaked overnight in milk in order to eat it.

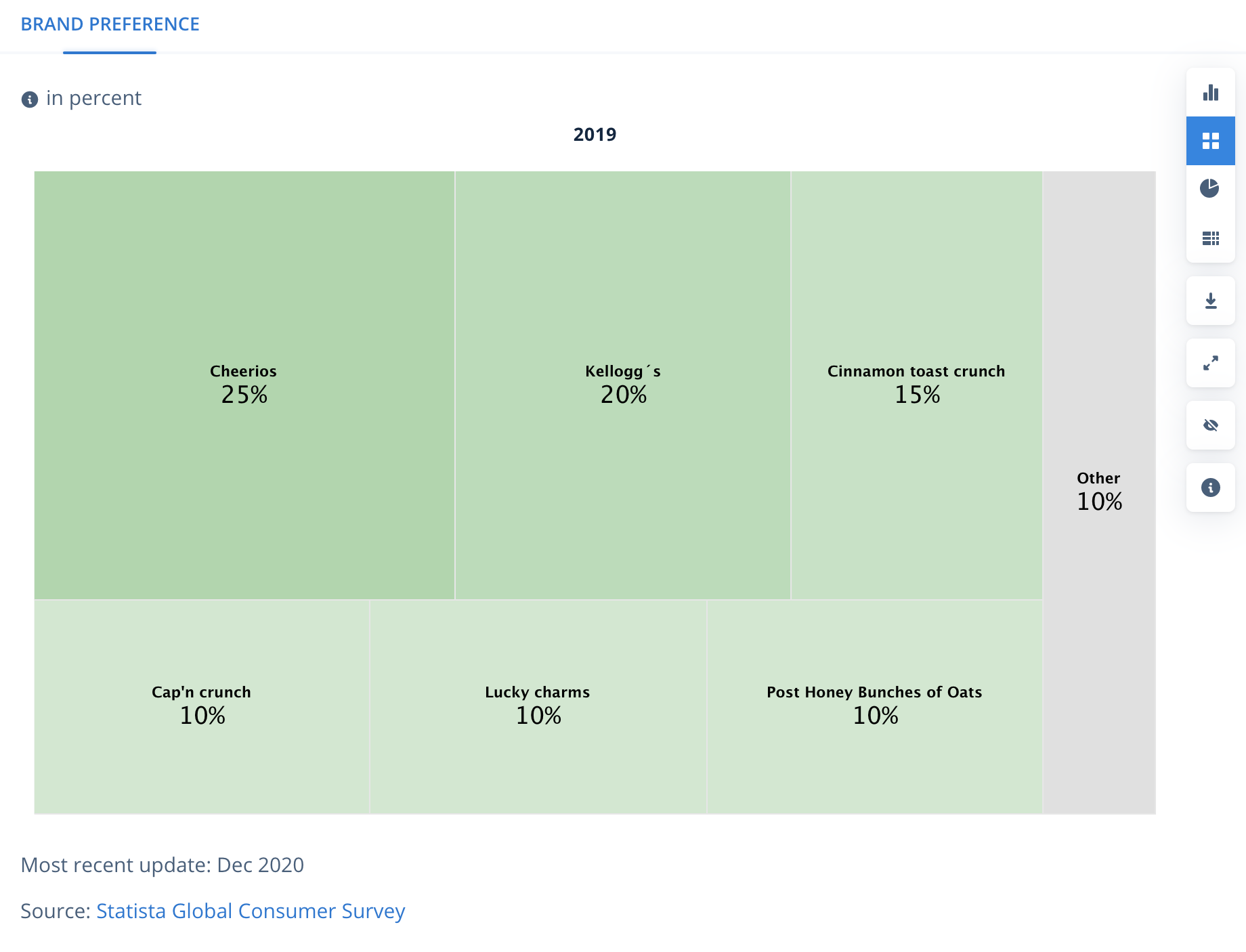

Cereal is dominated by four major players: Kellogg’s, General Mills, Post, and Quaker Oats. Really, though, Kellogg’s and General Mills are the gigantic players. In a consumer preference survey, Statista found that Kellogg’s and Cheerios (General Mills) represented 45% of consumer preference for cereals.

Another way of visualizing the prevalence of a brand like Kellogg’s is to walk through the cereal aisle of the grocery store. It probably looks a bit like this:

That kind of shelf prominence is important because most cereal is still bought in a store. That last sentence may sound obvious, but it’s worth a moment of reflection.

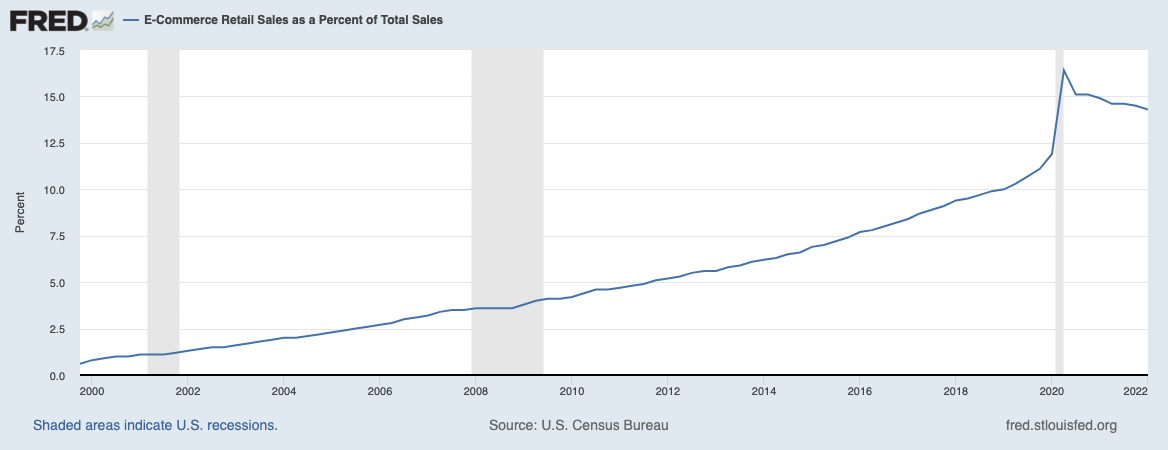

Retail sales are still prominently done in a physical store. But sales conducted online have gradually increased, with a pop during the height of the COVID-19 pandemic in Q2 2020, but represent only about 14% of total retail sales.

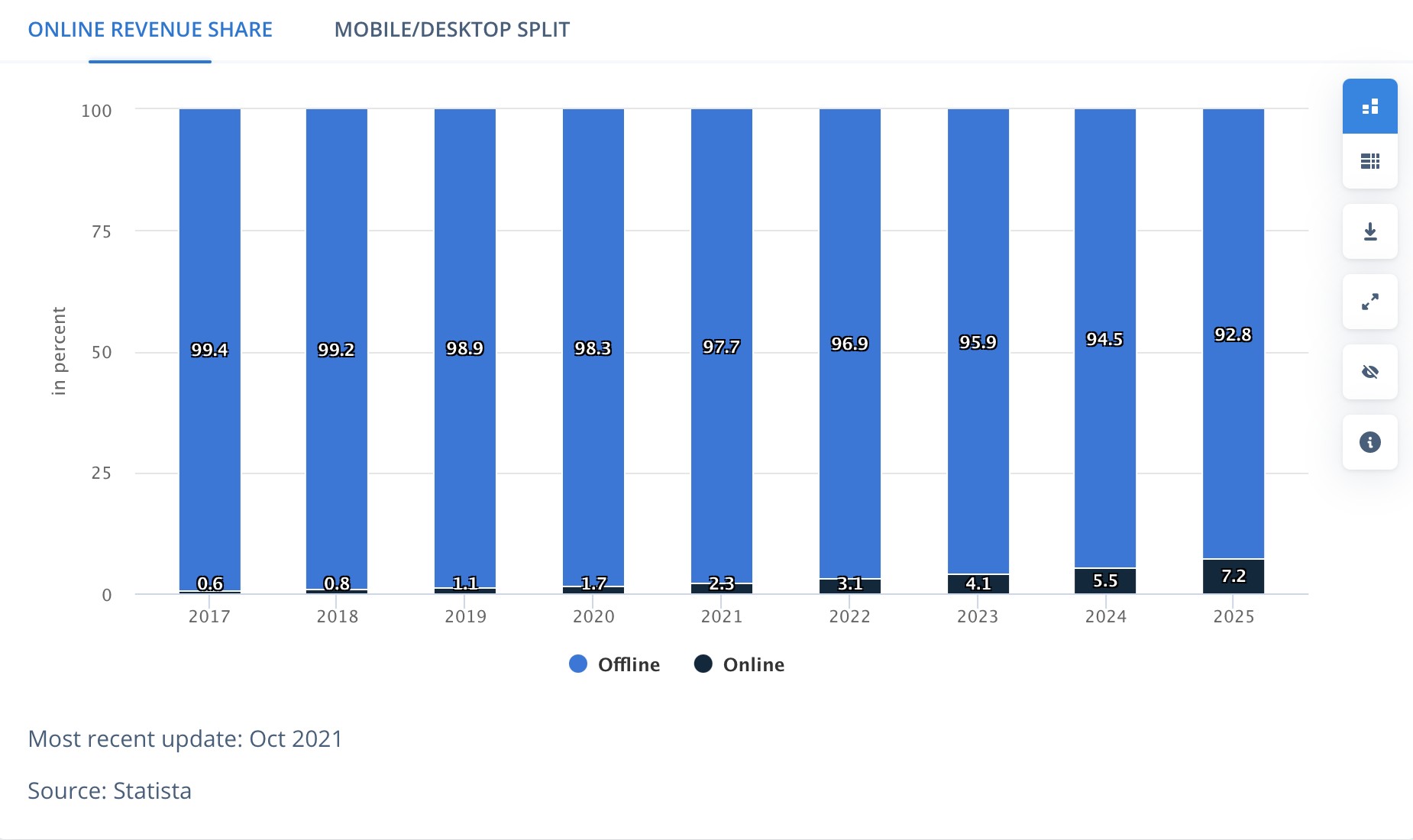

But groceries lag even other retail sales for online shopping. Because of COVID-19 eCommerce jumped as a percentage, but still represents only about 7-8% of total grocery retail sales. And cereal lags even that with online sales representing a tiny sliver of total retail sales.

You would think those percentages and shelf space would make legacy players invincible. That’s a matter of perspective. Because the cereal business is undergoing some major shifts that the DTC disruptors believe make the Goliaths vulnerable to a well-aimed rock. The three biggest being sluggish sales, consumer tastes, and pricing problems.

Flattening the Cereal Curve

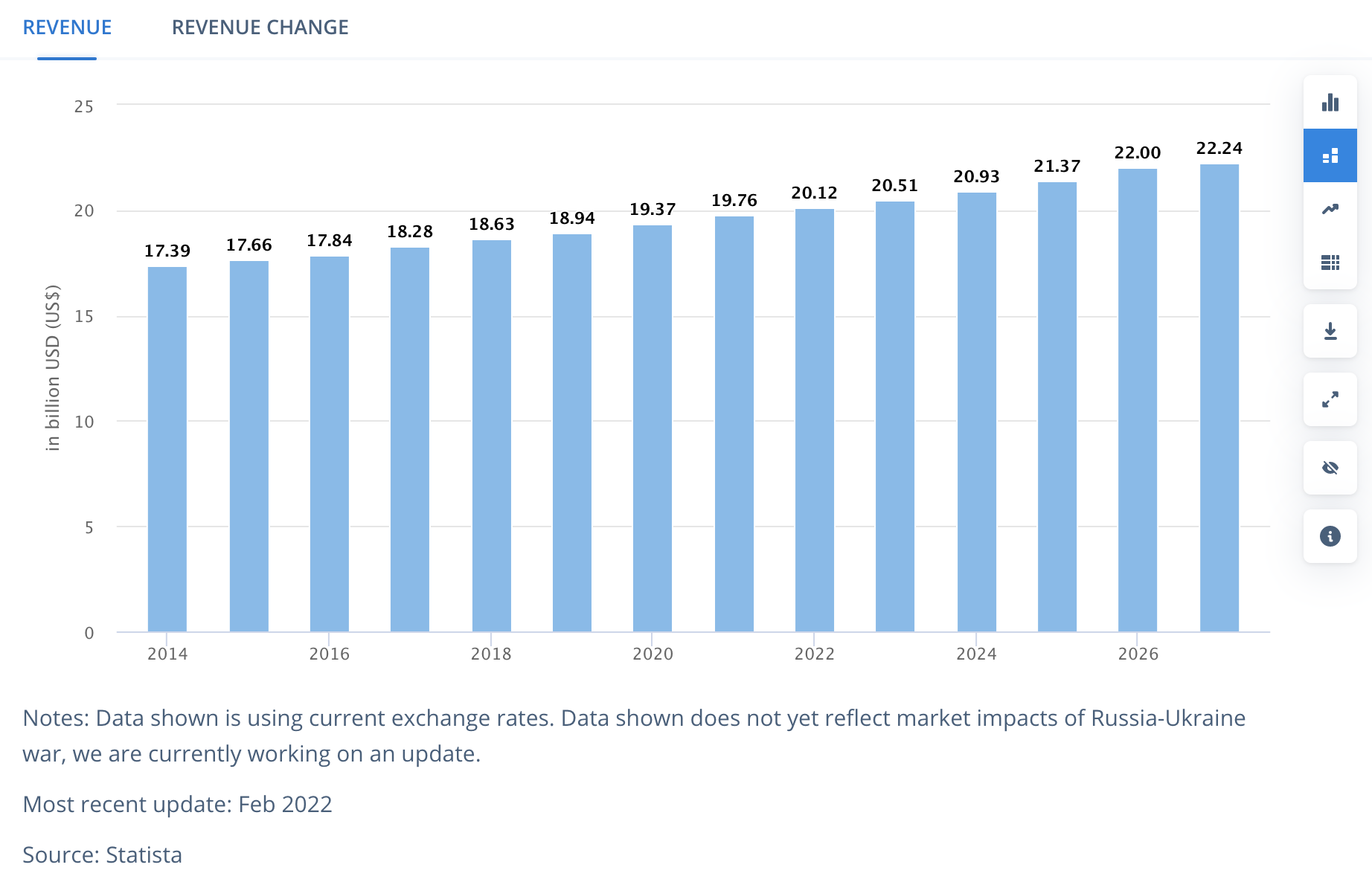

Globally, cereal sales represent about a $20 billion market, growing around 2%, according to Statista. A nice business, but if you’re feeling the pressure for fast growth, not an amazing one.

This is one of the reasons why conglomerates like Kellogg’s and General Mills have been so busy acquiring over the past decade. General Mills has paid billions to get into the pet food market. In the decade since Kellogg’s dropped nearly $3 billion for the Pringles brand, snack foods are now its biggest business at $11.4 billion in net sales last year compared to cereal net sales of $2.4 billion. The difference in growth and market size is so stark that General Mills restructured its company, and Kellogg’s recently announced it will split into three separate companies.

The big names in cereal are diversifying to the point that their core focus is other markets. That leaves the potential for DTC upstarts to come in and eat market share, particularly when you consider our next trend.

Sugar(less) High

Saying sugar is associated with cereal is an understatement. An average serving of cereal contains 20 grams of sugar. By comparison, a Krispy Kreme donut has 10 grams of sugar. Not all cereal is saturated with sugar, but the market overall is synonymous with cartoon characters and sweets. That’s more and more out of step with consumer preferences, particularly among millennials and Gen Z.

Increasingly health-conscious consumers are spurning the sugar in favor of the protein. And it’s not that there aren’t cereal brands that are healthier, but it’s hard to market nostalgia with modified Grape Nuts.

Many of the new entrants in the market are specifically targeting people following or dabbling in Paleo and Keto diets. These are often associated with low sugar, lots of protein, and younger consumers. One survey found that consumers between 18 and 34 years old were more than twice as likely to try Paleo as those 55 years old or older.

The cereal upstarts are aware of these trends, producing cereals that feature low-sugar to no-sugar, but in packaging and product that recalls Saturday mornings in front of the tube rather than dull-flavored bran.

The Cost of the Goods

It’s never easy to break into an established market. It’s even harder when the product is physical and edible. One of the biggest obstacles is finding a price point that is profitable while being palatable to a consumer used to a low cost achieved through the scale of a massive conglomerate.

These are the headwinds the upstarts face, most of which charge a premium over the price standard at the grocery store. (OffLimits and Magic Spoon are between $8.50 and $10 per box; Schoolyard Snacks is around $2 per single-serving bag, but you have to buy at least a bundle of 12 bags at $32.99 for a one-time purchase.)

The sticker shock may seem insurmountable. But the headwinds facing the big brands suggest it may be less of an issue. Between the supply chain issues of COVID-19 and the price hikes of ingredients like wheat due to Russia’s invasion of Ukraine, prices continue to rise for the major cereal-makers. And those are getting passed down to the consumer.

The gap in price between the big brands and the DTC brands is still wide but narrowing. And when combined with a cheaper marketing strategy and a product more in line with consumer demands that price point may not be enough to keep them from eating market share.

Boxing Out the Competition

It’s easy to brush off DTC brands with some funding, celebrity endorsements, and some social media buzz as unlikely to unseat Kellogg’s, General Mills, or even Post from the cereal throne. After all, those companies earn billions in dollars largely from entrenched spots on the coveted grocery store shelves.

But this really depends on your perspective. Those who dominate the cereal industry are experiencing supply chain issues, rising inflation, a product that may not match the tastes of the next generation of consumers, and a bevy of product lines outside of cereal that are stealing their focus. For the upstarts, the plan isn’t to win overnight. It’s to command a larger share of the bowl.

To pull that off, they’ll need to not only win against the big brands, but against each other. That’s why in our Mystery Shopper series, we’ll be looking at the strategy and tactics of three of them from a consumer’s perspective. We’ll examine their creative, targeting, messaging, and marketing channel strategies. And, yes, sampling their products.

The goal is to learn how they’re applying eCommerce and DTC approaches to a massive, entrenched industry, as well as how they differ in approach. Sign up to get our newsletter as we “cereal-ize” the content. (Sorry, couldn’t resist.)